FDIC-Insured

- Backed by the full faith and credit of the U.S. Government

To report a lost or stolen debit card please call 1.888.577.0404 during normal operating hours. After hours, please call 1.800.500.1044 immediately or access www.visa.com

Our Bank Routing and Transit Number is: 063114661

You will be linking to another website not owned or operated by Cogent Bank. Cogent Bank is not responsible for the availability or content of this website and does not represent either the linked website or you, should you enter into a transaction. The inclusion of any hyperlink does not imply any endorsement, investigation, verification or monitoring by Cogent Bank of any information in any hyperlinked site. We encourage you to review their privacy and security policies which may differ from Cogent Bank.

If you "Proceed", the link will open in a new window.

You are leaving Cogent Bank and going to Cogent Private Wealth, a boutique advisory firm offering comprehensive financial planning and investment management services. Some of their products are NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY; NOT GUARANTEED BY THE BANK; and MAY LOSE VALUE.

If you "Proceed", the link will open in a new window.

Please note that by clicking on this email address, you are leaving the Cogent Bank website and accessing an external email platform. Cogent Bank has no control over the content of any communications contained within this platform and cannot be held responsible for any information exchanged. We caution users to be careful when sharing any personal or sensitive information via email, as it may be intercepted or misused by third parties. By using this email platform, you accept full responsibility for any risks that may arise from its use.

If you "Proceed", the link will open in a new window.

While the news cycle may have moved on from Hurricane Ian, Southwest Floridians are still digging out, assessing the damage, and trying to get back on their feet. From lost or damaged homes and vehicles to lost jobs, the financial effects of a disaster can be as hard to deal with as the physical damage. In this article, we’ll walk you through the steps to recover financially from a disaster. Keep in mind that the road ahead may be long. Luckily, you’re not alone in walking it as neighbors, businesses, charities, and government agencies are working together to help Southwest Florida recover and rebuild. As you follow these steps, be sure to take care of your physical, emotional, and mental health. Exercise caution when returning to a damaged home or business and give yourself time to rest.

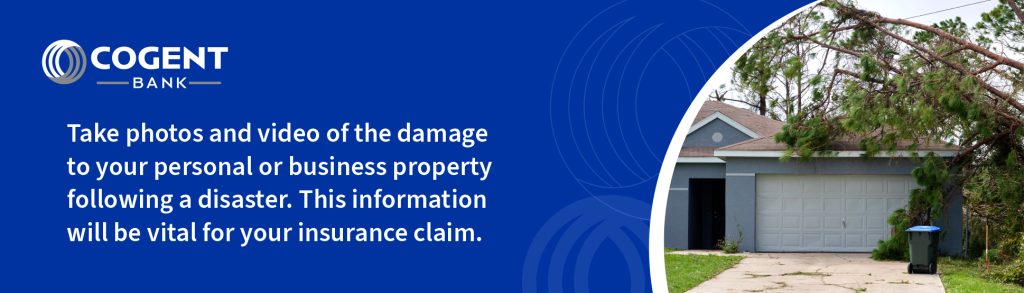

If possible, take pictures and videos of the damage done to your property after the disaster. This will be vital for insurance purposes. Don’t just leave the documentation on your smartphone; email the photos and videos to yourself or otherwise back them up so you won’t lose them.

In addition to the physical damage done to your home or business, make a list of damaged vehicles, furniture, electronics, and other personal or business property. You should also keep these items until the insurance adjustor has had a chance to review them.

If your home was rendered uninhabitable, hold on to receipts for temporary living expenses such as hotel stays, food, transportation, and storage.

You can make repairs that are “reasonable and necessary” such as covering holes to prevent additional damage to your home or business. Just document these temporary fixes and save the receipts for any materials you purchased. Wait until your claim is processed before making more permanent and extensive repairs.

If you or members of your family were injured in the disaster, you’ll want to collect records of medical treatment, tests or scans, and follow-up appointments. In the worst-case scenario, if a family member died in the disaster, you’ll need a copy of the death certificate to file a claim on their life insurance policy.

Once you’ve collected all your documentation, it’s time to file a claim. You may need to file more than one claim depending on the damage you sustained. For example, if both your home and your vehicle were damaged in the disaster, you’ll need to file separate claims with your home and auto insurers. Keep in mind that insurance companies will be experiencing higher than normal demand after a disaster, so you may have to wait longer than usual for an appointment with a claims adjustor.

Once the claims adjustor has finished the evaluation, you should receive a scope of loss document that details the type and amount of damage done, plus the cost of materials and labor needed to repair or rebuild. In the case of a damaged vehicle, your car may be a “total loss,” meaning the insurance company will pay you its current market value.

Pay attention to the amount of money your insurer offers to repair or replace your home. Will it cover the total cost? If not, you may need to provide additional documentation of your home’s condition before the disaster such as interior and exterior photos, a floor plan sketch, and proof of any recent improvements.

Whether you’re filing a personal or business claim, it’s best to get started as soon as possible so your claims will be processed faster, and you can get back on your feet sooner. This can be a time-consuming process, with claims addressed in the order they were received. This is especially true during a widespread disaster like a hurricane, when so many people will be contacting their insurance companies. Although it may feel overwhelming, don’t delay.

Once you have the ball rolling with your insurance claims, it’s a good idea to review your overall financial situation. You should know how much you have in savings, what your current cash flow looks like, and identify any steps you can take to improve things. For example, you may need to cut back on unnecessary expenses until your finances have recovered. If you lost your job in the disaster or are experiencing a temporary loss of income, you’ll also need to contact your creditors and utility companies to see if they can offer any assistance by temporarily reducing or pausing payments. Many creditors are willing to work with people impacted by a disaster, particularly if you contact them before payments are due. That’s why it’s so important to reach out proactively as soon as you can. Need help with a Cogent Bank account or loan? You can contact us here.

If you keep any important information at home, such as bank statements, birth certificates, passports, and so on, you will want to recover these documents if you can. Take precautions while cleaning up and locating any valuables. If you don’t use one already, you may want to invest in a safe that is designed to withstand extreme conditions such as fire and water damage.

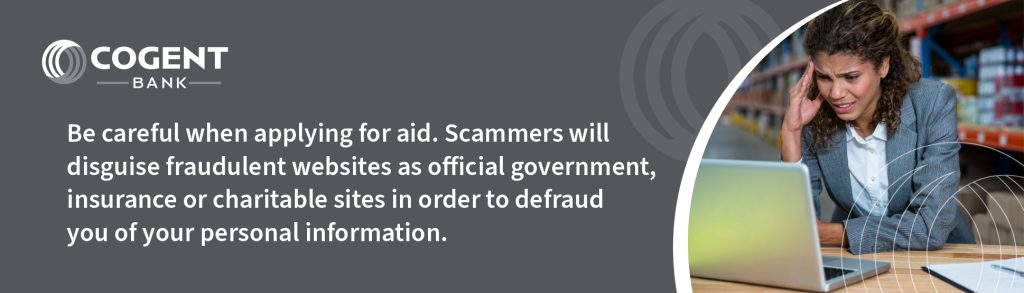

Regardless of your personal resources, you should apply for assistance from charities and government agencies working on the ground to provide help. You may be able to qualify for assistance with food, bills, unemployment, tax relief, and more. Just look out for scams and fraud; be cautious when browsing websites and check that they contain .gov at the end of the web address (if it’s an official government agency or website). Also be careful when looking at emails you receive purporting to be from government agencies, insurance companies, etc. The following agencies and organizations are recommended for assistance after a disaster:

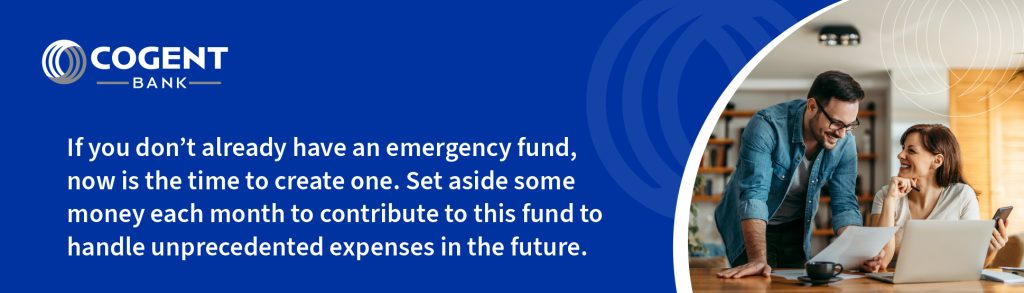

Damage from a natural disaster like a hurricane is a valid reason to dip into your emergency fund. Don’t have an emergency savings account? Now–or as soon as you get back on your feet–is the time to build one. Use our Savings Goal Calculator to figure out how much you’d need to save each month to reach your total goal (such as three months of living expenses) in a certain amount of time. Even if you can only put away a small amount of money each month, it will eventually add up and be there to help you when you need it most. If you’re a small business owner, you should also have an emergency savings for your business.

At Cogent Bank, we are dedicated to Moving You Forward. If you have questions about your bank or loan account or anything else, call us to set up an appointment or reach out to your Relationship Manager. For more help recovering from Hurricane Ian, check out our recent blog article on how to detect and avoid disaster scams in Florida.

The information contained herein is for informational/educational purposes only. The views and opinions expressed in this document may be those of the individuals and may not necessarily reflect those of Cogent Bancorp and its subsidiaries and affiliates, or the entities they may represent. Content contained herein may be used in connection with the advertising and/or marketing of products offered by Cogent Bank or Cogent Private Wealth. The material is not intended to provide or substitute for legal, tax, or financial advice or to indicate the availability or suitability of any Cogent Bank product or service. You should consult with a legal, financial, tax, or other appropriate professional(s) for your specific needs and/or objectives before making any decisions.